Dealing with Business Debt: How to Wind Up Your Own Company: A Guide for Directors and Shareholders on Liquidation Procedures

This guide is designed for directors and shareholders who need clear, practical advice on winding up a limited company. It provides step-by-step information about liquidation procedures, including the roles and responsibilities of directors, what to expect during the process, and legal considerations. We are able to discuss and advise on 0800 1804 933.

Who Is This Guide For?

- Directors of insolvent companies seeking an orderly closure.

- Shareholders needing to understand the liquidation process.

- Creditors wanting insight into their rights and recovery options.

What Does This Guide Cover?

- Liquidation Explained: A breakdown of what liquidation involves, the types available, and how each process works.

- DS01 Form Completion

- Voluntary vs Compulsory Liquidation: Clear distinctions to help you choose the right approach.

- Director Responsibilities: Legal duties, potential liabilities, and conduct reviews.

- Practical Steps: Checklists and actionable advice to simplify decision-making.

- Impact on Creditors and Employees: Explains how liquidation affects these stakeholders.

- Alternatives to Liquidation: Options to consider if your company’s situation permits recovery.

How to Use This Guide

- Assess Your Situation: Start by identifying whether your company is insolvent.

- Choose a Path: Use the detailed sections to explore voluntary or compulsory liquidation options.

- Take Action: Follow the practical advice and checklists to meet your legal obligations and ensure a smooth process.

- Get Professional Help: This guide complements the advice of legal or insolvency professionals. Always consult a licensed insolvency practitioner for personalised guidance. At Anderson Brookes we have our own in-house licensed IP ready to support and advice.

Free Consultation – advice@andersonbrookes.co.uk or call on 0800 1804 933 our freephone number (including from mobiles).

Overview

Liquidation is a formal legal process used to wind up a company’s affairs, often when it can no longer pay its debts or has reached the end of its purpose. It’s not just about closing the business – it’s about ensuring everything is handled properly, from settling debts to managing remaining assets. Whether your company is solvent or insolvent, understanding the process and your options is critical to making informed decisions.

How to Wind Up Your Own Company: The DS01 Procedure

As a director or shareholder, you may choose to wind up your company voluntarily if it has ceased trading or has no further purpose. If someone is considering a DIY approach then quite often it is with a DS01 form. This procedure is also known as striking off or dissolving the company.

The DS01 procedure is a simple and cost-effective way to remove a company from the Companies House register, provided that certain eligibility criteria are met. To be eligible for the DS01 procedure, your company must:

- Not have traded or carried on business in the last 3 months

- Not have changed its name in the last 3 months

- Not be threatened with liquidation or have any agreements in place with creditors, such as a Company Voluntary Arrangement (CVA)

Before applying for the DS01 procedure, it’s essential to ensure that your company has:

- Settled all outstanding bills and debts. This is often the biggest reason it doesn’t work.

- Closed any company bank accounts and distributed any remaining assets to shareholders

- Filed all necessary tax returns and paid any outstanding tax liabilities

- Informed all stakeholders, including shareholders, employees, and creditors, of the intention to dissolve the company

To apply for the DS01 procedure, you must complete and submit form DS01 to Companies House, along with the required fee (£33). The form can be submitted online or by post, although online submissions are generally processed more quickly.

It’s crucial to ensure that the form is completed accurately and signed by the majority of the company’s directors. Incomplete or incorrect forms may be rejected, causing delays in the striking off process.

Once the DS01 form is processed, Companies House will publish a notice in the Gazette, giving interested parties the opportunity to object to the proposed striking off. If no objections are received within 2 months, the company will be struck off the register and cease to exist as a legal entity.

While the DS01 procedure can be a straightforward way to wind up a company, it’s important to seek professional advice to ensure that it is the most appropriate option for your circumstances. Improperly closing a company can lead to future issues, such as personal liability for directors or difficulty in starting a new business. We are here to help.

What is Liquidation?

Liquidation is the process of legally dissolving a limited company. During this process, a licensed insolvency practitioner, known as the liquidator, takes control of the company’s affairs. Their role is to ensure the company’s obligations are met as far as possible. This includes:

- Completing or terminating any outstanding contracts.

- Selling off company assets to repay creditors.

- Handling legal disputes.

- Returning any surplus funds to shareholders (if applicable).

Once these tasks are complete, the company is removed from the Companies House register and ceases to exist as a legal entity.

It’s important to note that liquidation doesn’t always mean creditors will be fully repaid. Instead, the goal is to handle the company’s remaining affairs in a structured, transparent manner.

What Types of Liquidation Are There?

There are three main types of liquidation, depending on the company’s financial position and the circumstances of its closure:

-

Members’ Voluntary Liquidation (MVL):

Used when a company is solvent and has sufficient assets to pay all debts. The directors must make a formal declaration of solvency, confirming the company can settle its debts within 12 months. MVL is often used for tax-efficient business closures – but of course not available to those with debts which can’t be paid.

-

Creditors’ Voluntary Liquidation (CVL):

When a company is insolvent and unable to pay its debts, directors can opt for a CVL. This process allows the company to close down in an orderly manner, with the liquidator distributing any remaining assets to creditors. See our CVL Timeline. Please note, Anderson Brookes can place a company into liquidation within 8 days.

-

Compulsory Liquidation:

This occurs when the court orders a company to be wound up, typically following a winding-up petition from creditors who are owed money. Compulsory liquidation removes control from the directors entirely, with the court-appointed liquidator taking over.

Where Can I Get Advice About Liquidation?

Before taking any steps, it’s essential to seek advice to understand your options fully. You can get reliable guidance from:

- A licensed insolvency practitioner, who will explain your legal obligations and the best course of action. We are here!

- Solicitors or qualified accountants familiar with insolvency law.

- Reputable financial advisers or debt support organisations, such as Citizens Advice.

If you’re uncertain about your next steps, Anderson Brookes is here to help. Our team of experts provides personalised advice, ensuring you understand your rights and responsibilities while identifying the best solution for your situation.

What Are the Alternatives to Liquidation?

Liquidation is not always the only option. Depending on your company’s financial position, there may be other paths to explore:

-

Informal Arrangement:

Negotiating directly with creditors to agree on payment terms without formal insolvency proceedings.

-

Company Voluntary Arrangement (CVA):

A structured agreement supervised by an insolvency practitioner, allowing the company to repay debts over time while continuing to trade.

-

Administration:

Offers temporary protection from creditor actions while an administrator restructures the business or sells its assets to achieve the best possible outcome for creditors.

Each option has its own advantages and implications, so professional advice is crucial in deciding the most appropriate course of action.

Why Understanding Liquidation Matters

For directors, the decision to enter liquidation is significant and often complex. Missteps, such as trading while insolvent or failing to act responsibly, can result in personal liability or disqualification. By understanding your options and acting decisively, you can fulfil your legal duties while protecting your interests.

Let us guide you through this challenging time. Anderson Brookes specialises in helping businesses and directors navigate liquidation and alternative solutions with confidence and clarity. Contact us for expert, tailored advice.

Voluntary Liquidation

Voluntary liquidation is a structured process initiated by the shareholders or directors of a company to wind up its affairs. Unlike compulsory liquidation, it is not enforced by the courts, giving directors and shareholders more control over the process. This route is often chosen to ensure an orderly closure of the company while fulfilling legal responsibilities and safeguarding reputations.

What Is Voluntary Liquidation?

Voluntary liquidation involves appointing a licensed insolvency practitioner to act as a liquidator, who will take charge of:

- Selling company assets to repay creditors.

- Settling any outstanding legal or financial obligations.

- Distributing any remaining funds (if applicable) to shareholders.

- Ensuring the company is dissolved and removed from the Companies House register.

There are two main types of voluntary liquidation, each tailored to the company’s financial position:

1. Members’ Voluntary Liquidation (MVL)

When to Consider MVL:

MVL is used when the company is solvent and has enough assets to pay all its debts, including interest, within 12 months. Directors often choose this option for tax-efficient closures, particularly when retiring, restructuring, or winding down operations no longer needed.

Key Steps in an MVL:

- Declaration of Solvency: Directors must formally confirm the company’s solvency after a thorough review of its finances.

- Shareholder Approval: Shareholders must pass a resolution (requiring a 75% majority) to wind up the company.

- Appointment of a Liquidator: A licensed insolvency practitioner is appointed to handle the process.

- Asset Distribution: Once debts are paid, any surplus funds are returned to shareholders.

Legal Obligation:

Making a false declaration of solvency without reasonable grounds is a criminal offence, so professional guidance is essential.

2. Creditors’ Voluntary Liquidation (CVL)

When to Consider CVL:

If the company is insolvent and cannot meet its financial obligations, a CVL enables directors to take proactive steps to close the business while prioritising creditors’ interests. This route demonstrates responsible leadership and minimises risks of personal liability.

Key Steps in a CVL:

- Director Decision: Directors agree that the company is insolvent and cannot continue trading.

- Shareholder Resolution: Shareholders vote to approve the CVL, requiring a 75% majority.

- Creditor Meeting: A meeting is convened where creditors can approve or nominate the liquidator.

- Liquidator’s Role: The liquidator oversees asset realisation, creditor payments (if funds allow), and legal compliance.

- Conduct Review: The liquidator submits a report on the directors’ conduct to the Secretary of State to identify any potential misconduct.

What Happens During Voluntary Liquidation?

Once the resolution is passed:

- The business ceases trading immediately unless essential activities are needed to support the liquidation process.

- Company assets are sold, and proceeds are distributed in a legally defined order of priority, starting with secured and preferential creditors.

Voluntary Liquidation Process

When Does Voluntary Liquidation End?

Voluntary liquidation concludes once:

- All assets have been realised.

- Creditors have been paid in accordance with the company’s financial capacity.

- Final meetings of shareholders (and creditors in a CVL) are held to confirm the closure of the company.

The company is then removed from the Companies House register and ceases to exist as a legal entity.

Why Choose Voluntary Liquidation?

Voluntary liquidation offers directors a way to:

- Take control of the process and avoid court enforcement.

- Fulfil their legal duties responsibly, reducing personal risks.

- Protect their professional reputation by managing creditor relationships effectively.

Anderson Brookes specialises in managing voluntary liquidations with transparency and efficiency. Whether you’re considering MVL for a solvent closure or CVL for an insolvent company, we provide expert support tailored to your situation. Contact us today for a free consultation.

Free Consultation – advice@andersonbrookes.co.uk or call on 0800 1804 933 our freephone number (including from mobiles).

Compulsory Liquidation

Compulsory liquidation is a court-ordered process that forces a company to close when it is unable to pay its debts or has committed other legal breaches. Unlike voluntary liquidation, the company’s directors do not initiate or control the process. Instead, a creditor, shareholder, or another party applies to the court for a winding-up order. This can be a challenging and stressful process for directors, making it vital to understand the procedure and your responsibilities.

What Is Compulsory Liquidation?

Compulsory liquidation begins when the court issues a winding-up order, often at the request of a creditor owed £750 or more. Once the order is granted, a liquidator is appointed to take control of the company. Their primary role is to:

- Sell off company assets to repay creditors.

- Distribute the proceeds in a legally determined order.

- Investigate the directors’ conduct leading up to insolvency.

- Dissolve the company at the end of the process.

This process is public, involves legal proceedings, and can damage the professional reputation of directors.

Who Can Apply for Compulsory Liquidation?

The following parties can petition the court for a winding-up order:

- Creditors – Most petitions are filed by creditors owed money.

- Shareholders – In rare cases, shareholders may petition to wind up a company if they believe it is acting against their interests.

- The Company – Directors may apply for compulsory liquidation if they are unable or unwilling to initiate a Creditors’ Voluntary Liquidation.

- The Secretary of State or Other Authorities – In cases of misconduct or public interest concerns, government agencies may request a winding-up order.

Key Steps in Compulsory Liquidation

- Filing a Petition: The creditor or petitioner submits a winding-up petition to the court, outlining the reasons for liquidation and providing evidence of the debt.

- Court Hearing: A hearing is held to determine whether the petition is valid. The company has an opportunity to challenge the petition if there are grounds to do so.

- Winding-Up Order Issued: If the court approves the petition, it issues a winding-up order. This removes the directors’ powers and appoints an Official Receiver or liquidator.

- Asset Realisation: The liquidator identifies, values, and sells company assets to raise funds for creditors.

- Creditor Distributions: Proceeds are distributed to creditors in a set legal order, starting with secured creditors and preferential claims (e.g., employee wages).

- Director Conduct Review: The liquidator investigates directors’ actions to determine if there was any wrongful or fraudulent trading.

- Dissolution of the Company: Once the liquidation is complete, the company is struck off the Companies House register and ceases to exist.

When Does Compulsory Liquidation Occur?

Compulsory liquidation is often the last resort when:

- Creditors are unable to recover money through standard means.

- Directors have failed to act responsibly or ignored creditor demands.

- The company’s financial position is unsalvageable.

Risks for Directors in Compulsory Liquidation

- Loss of Control:

Directors lose authority immediately after the winding-up order, with the liquidator taking over all decision-making, as noted above.

- Legal and Financial Risks:

Directors may face personal liability for debts if they engaged in wrongful trading or signed personal guarantees.

- Conduct Review:

Misconduct can lead to disqualification from acting as a director for up to 15 years.

- Reputational Damage:

Compulsory liquidation is a public process that can impact professional credibility.

Minimising the Risks of Compulsory Liquidation

If you are concerned about compulsory liquidation, consider taking proactive steps:

- Respond promptly to creditor demands.

- Seek professional advice to explore alternatives, such as a Creditors’ Voluntary Liquidation or repayment agreements.

- Provide accurate financial records and cooperate fully with the liquidator.

By acting early, you may be able to protect your interests and ensure a smoother resolution.

Checklist for Directors Before Liquidation

For directors, preparing for liquidation is not just about complying with legal requirements—it’s about demonstrating responsibility, protecting creditors’ interests, and safeguarding your own reputation. This checklist outlines the essential actions you must take before initiating liquidation to ensure a smooth and compliant process.

1. Confirm the Company’s Financial Position

- Assess Solvency: Determine if the company is insolvent by reviewing cash flow and balance sheet indicators. Seek professional advice if unsure.

- Identify Debts: Compile a complete list of creditors, including amounts owed and due dates.

- Review Assets: Document all company assets, including property, equipment, inventory, and intellectual property.

2. Stop Trading If Insolvent

- Cease Operations: If the company cannot meet its obligations, stop trading immediately to avoid accusations of wrongful trading.

- Avoid New Liabilities: Do not incur additional debts, as this could lead to personal liability.

3. Inform Stakeholders

- Communicate with Directors and Shareholders: Hold a board meeting to discuss the company’s position and agree on the next steps.

- Notify Employees: Let staff know about the situation, including timelines and redundancy rights. Provide updates as soon as decisions are finalised.

4. Gather Financial Records

Ensure all documentation is up to date, accurate, and ready to share with the insolvency practitioner. Key documents include:

-

- Financial statements.

- Recent bank statements.

- Tax records (VAT, PAYE, corporation tax).

- Aged creditor and debtor lists.

- Asset valuations.

- Employee payroll records.

5. Seek Professional Advice

- Appoint an Insolvency Practitioner: Engage a licensed practitioner to guide you through the liquidation process and manage creditor communications.

- Discuss Options: Explore alternatives, such as a Company Voluntary Arrangement (CVA) or administration, if appropriate.

- Understand Your Duties: Ensure you’re clear on your responsibilities during liquidation and what’s required to comply with the law.

6. Protect Your Position as a Director

- Act Transparently: Provide full cooperation to the liquidator and disclose all relevant information.

- Avoid Misconduct: Do not prioritise certain creditors over others or attempt to hide assets.

- Prepare for a Conduct Review: Understand that the liquidator will review your actions leading up to insolvency to ensure compliance with legal obligations.

7. Plan for Post-Liquidation

- Consider Personal Liabilities: Understand how personal guarantees or outstanding director loans may affect you.

- Prepare for Rebuilding: If you plan to start a new business, ensure you comply with phoenix company rules and take steps to restore your creditworthiness.

Why Preparation Matters

By following this checklist, directors can minimise risks, fulfil their legal duties, and ensure the liquidation process runs as smoothly as possible. Early action demonstrates responsible leadership, helping to protect your reputation and reduce the likelihood of personal liability.

Common Mistakes to Avoid During Liquidation

Liquidation is a complex process, and directors must take extra care to avoid actions that could complicate matters or lead to legal and financial repercussions. Mistakes during this time can damage your professional reputation, result in personal liability, or even lead to disqualification as a director. Understanding these pitfalls can help you navigate liquidation responsibly and with confidence.

1. Continuing to Trade While Insolvent

- The Mistake: Allowing the company to continue trading when you know it cannot pay its debts.

- Why It’s an Issue: This is considered wrongful trading and can lead to personal liability for additional creditor losses.

- How to Avoid It: Cease trading immediately once insolvency is identified, and consult an insolvency practitioner for guidance.

2. Favouring Certain Creditors

- The Mistake: Repaying some creditors, such as suppliers or family members, ahead of others.

- Why It’s an Issue: This breaches the principle of creditor equality and could be viewed as misconduct.

- How to Avoid It: Allow the liquidator to manage all creditor payments as part of the formal liquidation process.

3. Delaying Action

- The Mistake: Waiting too long to address financial issues or initiate liquidation.

- Why It’s an Issue: Delays can worsen the company’s financial position, increase creditor pressure, and heighten risks of personal liability for directors.

- How to Avoid It: Act promptly at the first signs of insolvency, seeking professional advice early.

4. Failing to Maintain Accurate Records

- The Mistake: Not having up-to-date financial statements, creditor lists, or asset registers.

- Why It’s an Issue: Poor record-keeping can delay the liquidation process and raise suspicion of negligence or misconduct.

- How to Avoid It: Ensure all company records are accurate and readily available for the insolvency practitioner.

5. Attempting to Hide Assets

- The Mistake: Transferring company assets to other entities or individuals to keep them out of the liquidation process.

- Why It’s an Issue: This is considered fraudulent and can lead to severe penalties, including criminal charges.

- How to Avoid It: Be fully transparent with the liquidator, disclosing all assets and transactions.

6. Ignoring Creditor Communication

- The Mistake: Failing to engage with creditors or provide updates on the company’s situation.

- Why It’s an Issue: This can damage relationships and lead to increased legal actions, such as a winding-up petition.

- How to Avoid It: Maintain clear and professional communication with creditors, even if you cannot meet their demands.

7. Misunderstanding Personal Liabilities

- The Mistake: Assuming that personal assets are always protected under a limited company structure.

- Why It’s an Issue: Personal guarantees on loans or credit agreements may still hold you liable for certain debts.

- How to Avoid It: Review all agreements for personal guarantees and seek professional advice to understand your risks.

8. Choosing the Wrong Insolvency Practitioner

- The Mistake: Appointing an inexperienced or unqualified insolvency practitioner.

- Why It’s an Issue: Poor guidance can result in delays, increased costs, or failure to meet legal requirements.

- How to Avoid It: Research practitioners thoroughly, focusing on their experience, credentials, and client reviews.

9. Mismanaging Employee Redundancies

- The Mistake: Failing to inform employees of their rights or pay owed wages and redundancy entitlements.

- Why It’s an Issue: Mishandling redundancies can lead to claims against the company or directors personally.

- How to Avoid It: Work closely with the liquidator to ensure employees receive the support and information they need.

10. Overlooking Post-Liquidation Obligations

- The Mistake: Assuming liquidation ends all responsibilities for directors.

- Why It’s an Issue: You may still need to cooperate with the liquidator, attend meetings, or provide additional information after the company is dissolved.

- How to Avoid It: Stay engaged with the process until it is formally concluded and ensure you fulfil all requests from the liquidator.

Why Avoiding These Mistakes Matters

Taking the right actions during liquidation isn’t just about meeting legal requirements – it’s about protecting your personal and professional future. Directors who act responsibly throughout the process are less likely to face penalties, disqualification, or damage to their reputation.

Free Consultation – advice@andersonbrookes.co.uk or call on 0800 1804 933 our freephone number (including from mobiles).

Impact on Directors

Entering liquidation has significant implications for directors, both professionally and personally. While the liquidation process is designed to address a company’s financial issues, directors must navigate legal, financial, and reputational challenges. Understanding these impacts is crucial to acting responsibly and protecting your interests.

1. Legal Responsibilities During Liquidation

Directors retain certain legal obligations throughout the liquidation process, even after they lose operational control of the company. Key responsibilities include:

- Providing Accurate Information: Directors must supply complete and up-to-date financial records to the liquidator, including details of assets, liabilities, and creditor information.

- Cooperating with the Liquidator: Full cooperation is required, including answering questions, attending meetings, and providing documentation promptly.

- Avoiding Misconduct: Directors must not prioritise specific creditors, trade while insolvent, or attempt to hide company assets, as these actions can result in penalties.

2. Conduct Review by the Liquidator

The appointed liquidator will assess the directors’ actions leading up to insolvency to identify any misconduct or negligence. This includes:

- Examining financial records and company decisions.

- Investigating transactions that may indicate wrongful or fraudulent trading.

- Reporting findings to the Insolvency Service and, if necessary, recommending disqualification.

Outcome:

If misconduct is found, directors may face:

- Disqualification: Bans from acting as a director for 2 to 15 years.

- Personal Liability: Being held personally responsible for company debts caused by wrongful trading or fraud.

- Criminal Charges: In severe cases, fraudulent activity can lead to prosecution.

3. Financial Implications

While directors of limited companies are generally not personally liable for company debts, there are exceptions:

- If directors signed personal guarantees for loans or credit facilities, they remain liable for those debts.

- Outstanding director’s loans must be repaid to the company as part of the liquidation process.

- Directors may face legal fees if creditors pursue claims or disputes during liquidation.

4. Reputational Impact

The liquidation process is public, and details are recorded at Companies House. Directors must be aware of potential reputational consequences:

- Failure to manage liquidation professionally can damage relationships with creditors, suppliers, and lenders.

- Misconduct or disqualification can harm future business opportunities and employment prospects.

Mitigation:

Acting transparently, cooperating with the liquidator, and taking proactive steps to protect creditors’ interests can preserve your reputation.

5. Opportunities for Recovery

While liquidation can be challenging, it also provides opportunities for directors to rebuild:

- Directors can start a new business unless restricted by disqualification. However, using the same or a similar name as the liquidated company requires compliance with phoenix company rules.

- Taking steps to address personal liabilities and demonstrate financial responsibility can restore your standing with lenders and other stakeholders.

- Many directors emerge from liquidation with valuable lessons that contribute to future business success.

Post-Liquidation Tax Obligations

Liquidation doesn’t eliminate a company’s tax responsibilities. Directors must ensure all tax matters are properly handled during and after the liquidation process to avoid complications or penalties. Understanding these obligations helps ensure compliance and allows directors to conclude the liquidation process responsibly.

1. Filing Final Tax Returns

Before liquidation is completed, the company must:

- Submit a Final Corporation Tax Return: The company’s final accounting period ends the day before liquidation begins. The liquidator will typically handle this submission, but directors are responsible for providing accurate financial information.

- Finalise VAT Returns: Any outstanding VAT returns must be submitted, including those covering the period leading up to liquidation.

- Complete PAYE Obligations: Payroll records must be finalised, and any outstanding PAYE payments must be addressed.

2. Paying Outstanding Tax Liabilities

- Corporation Tax: Any corporation tax liabilities up to the point of liquidation are included in the company’s debts.

- VAT and PAYE: These taxes are considered preferential debts, meaning they are prioritised in the liquidation process.

- Tax Penalties: If there are overdue payments or penalties, these will also form part of the company’s liabilities.

Key Point: Directors are not personally liable for company taxes unless they signed personal guarantees or engaged in wrongful trading.

3. Liquidator’s Role in Tax Compliance

Once appointed, the liquidator assumes responsibility for managing the company’s tax affairs, including:

- Liaising with HMRC regarding outstanding taxes.

- Preparing and submitting final tax returns.

- Settling tax debts from the proceeds of asset realisation.

4. Tax Treatment of Asset Sales

The liquidator will sell the company’s assets to generate funds for creditors. These transactions may have tax implications:

- Capital Gains Tax: Chargeable gains from asset sales are assessed, and corporation tax is applied accordingly.

- Deductible Liquidation Costs: Costs directly associated with the liquidation process, such as liquidator fees and legal expenses, may be deducted when calculating taxable gains.

5. Tax Obligations for Directors

While directors are not usually liable for company tax debts, there are exceptions:

- Personal Guarantees: Directors may be personally responsible for tax liabilities if guarantees were provided to secure funding.

- Director’s Loan Accounts: Any outstanding director’s loans are treated as assets of the company and must be repaid, which can have personal tax implications.

6. Post-Liquidation Communication with HMRC

Even after the company is dissolved, HMRC may conduct follow-up investigations or require additional information regarding pre-liquidation activities. Directors should:

- Retain financial records for at least six years.

- Respond promptly to any HMRC inquiries to avoid delays or penalties.

7. Common Tax Pitfalls to Avoid

- Failing to Provide Accurate Information: Incomplete or inaccurate financial records can lead to disputes with HMRC.

- Overlooking Tax Liabilities: Neglecting PAYE or VAT obligations can result in penalties that complicate the liquidation process.

- Misunderstanding Tax Deductibility: Ensure all allowable expenses are claimed correctly to reduce taxable liabilities.

Why Tax Compliance Matters

Handling tax obligations correctly during liquidation ensures a smooth process and reduces the risk of legal or financial complications for both the company and its directors. By cooperating fully with the liquidator and HMRC, directors can fulfil their duties and move forward with confidence.

Rebuilding After Liquidation

Liquidation is undoubtedly a challenging experience for any director, but it doesn’t have to define your future. Many directors use it as a turning point—a moment to reflect, regroup, and rebuild. This process begins with understanding the lessons learned, addressing outstanding obligations, and planning your next steps with clarity and purpose.

Reflecting on the Past

The first step in moving forward is to take an honest look at what happened. Liquidation provides valuable lessons, whether related to financial management, risk planning, or external market forces. Consider what contributed to the company’s insolvency—was it cash flow pressures, insufficient contingency planning, or sudden external events? Recognising these factors helps avoid repeating mistakes. Equally, acknowledge the successes within your business. This balanced perspective is essential for rebuilding with confidence and focus.

Addressing Financial Obligations

After liquidation, directors must deal with any personal liabilities left behind:

- Personal Guarantees: If you provided guarantees for loans or credit, these debts remain your responsibility even after liquidation. Engaging with creditors to negotiate manageable repayment terms is crucial.

- Director’s Loans: Outstanding loans owed to the company must be repaid to avoid legal complications. This may feel burdensome, but resolving these obligations is a key step in restoring financial stability.

Dealing with these commitments head-on signals responsibility and begins the process of restoring trust with creditors and lenders.

Restoring Creditworthiness

Liquidation can impact your credit profile, but this doesn’t mean permanent damage. Steps to rebuild include:

- Reviewing your credit report and correcting any inaccuracies.

- Demonstrating financial reliability by paying existing debts on time.

- Separating personal and business finances in any future ventures to establish a clean financial history.

Rebuilding credit may take time, but it’s an important foundation for moving forward, whether as an entrepreneur or in other roles.

Planning Your Next Steps

For directors looking to start a new business, liquidation offers a chance to approach things differently. Creating a robust, risk-aware business plan will be essential, particularly if past challenges were linked to poor cash flow management or unexpected expenses. If you intend to use the same or a similar name as your liquidated company, ensure compliance with phoenix company rules under the Insolvency Act.

Not all directors return to entrepreneurship. Some choose to pursue employment opportunities where they can apply the skills gained through managing a business. Transparency is important—if asked about the liquidation, focus on how the experience has strengthened your decision-making and leadership abilities. Many employers value resilience and adaptability, which are often forged in tough circumstances like these.

Emotional Recovery

The stress of liquidation can take a toll, but addressing this is just as important as rebuilding financially. Seeking professional counselling or joining support networks can provide perspective and help you process the emotional impact. Connecting with others who’ve faced similar challenges often leads to valuable advice and encouragement.

Rebuilding Your Reputation

Liquidation doesn’t have to damage your professional credibility if you handle the process responsibly:

- Cooperate fully with the liquidator and creditors.

- Maintain clear communication with stakeholders, showing respect for their position.

- Seek professional certifications or further training to reinforce your standing in your industry.

By acting with integrity, you demonstrate professionalism and lay the groundwork for future opportunities.

Looking Ahead

Rebuilding after liquidation is a gradual process, but it’s also an opportunity for growth. Whether you plan to start a new business, pursue a different career, or simply reflect on the experience, this chapter can mark a fresh beginning. With careful planning, financial discipline, and the right support, liquidation can become a stepping stone to future success.

How to Choose the Right Insolvency Practitioner

Choosing the right insolvency practitioner (IP) is one of the most important decisions you’ll make when navigating liquidation. The IP not only manages the legal and financial aspects of the process but also ensures that you, your creditors, and other stakeholders are treated fairly. A skilled and experienced practitioner can make the process smoother, more efficient, and less stressful, so it’s important to select carefully.

Understanding the Role of an Insolvency Practitioner

An insolvency practitioner is a licensed professional who oversees the liquidation process. Their responsibilities include:

- Assessing the company’s financial position and advising on the best course of action.

- Managing creditor communication and ensuring legal compliance.

- Selling company assets to repay creditors.

- Conducting a review of directors’ conduct before and during insolvency.

Because the IP assumes full control of the liquidation process, directors must be confident in their choice and ensure the practitioner aligns with their needs.

Key Factors to Consider When Choosing an IP

Selecting an insolvency practitioner requires careful evaluation. Here are the critical factors to consider:

- Experience and Expertise

- Look for an IP with a proven track record in handling cases similar to your company’s situation.

- Industry-specific experience is especially valuable if your business operates in a niche or regulated sector.

- Qualifications

- Ensure the practitioner is licensed by a recognised body, such as ICAEW, IPA, or ICAS. Like our in-house IP at Anderson Brookes!

- Check their credentials and verify their standing with the appropriate regulatory body.

- Transparency and Communication

- The IP should explain the process clearly, including timelines, costs, and potential outcomes.

- Look for someone who communicates openly and provides regular updates.

- Cost and Fee Structure

- Understand their fee structure upfront. Ask for a detailed breakdown to avoid hidden costs.

- Compare quotes from multiple practitioners to ensure value for money, but be wary of choosing solely based on cost—quality and expertise matter.

- Reputation

- Research client reviews, case studies, or testimonials to gauge their professionalism and reliability.

- Word-of-mouth recommendations from trusted advisors, such as accountants or solicitors, can be invaluable.

- Approachability and Rapport

- The liquidation process can be emotionally challenging. Choose an IP you feel comfortable with and who demonstrates empathy and understanding.

Questions to Ask a Potential IP

Before appointing an insolvency practitioner, consider asking:

- What is your experience with companies in my industry or financial position?

- Can you provide references or case studies from similar cases?

- How will you communicate progress and handle creditor relationships?

- What are the total costs involved, and how are these calculated?

- What support will you provide to directors throughout the process?

These questions will help you assess whether the practitioner is the right fit for your needs.

The Risks of Choosing the Wrong IP

Selecting an inexperienced or unsuitable IP can lead to delays, increased costs, and additional stress. Worse, poor management of the liquidation process could result in unnecessary disputes with creditors or complications in legal compliance. By taking the time to choose wisely, you avoid these pitfalls and ensure the best possible outcome. We can place a company into liquidation within 8 days.

![]()

How Anderson Brookes Can Help

At Anderson Brookes, our team of licensed insolvency practitioners combines extensive experience with a commitment to clear, empathetic communication. We specialise in tailoring our approach to your company’s unique circumstances, ensuring a smooth and professional process from start to finish.

If you’re unsure where to begin, we’re here to provide guidance and help you make the right decision. Contact us today to discuss your options in confidence.

Free Consultation – advice@andersonbrookes.co.uk or call on 0800 1804 933 our freephone number (including from mobiles).

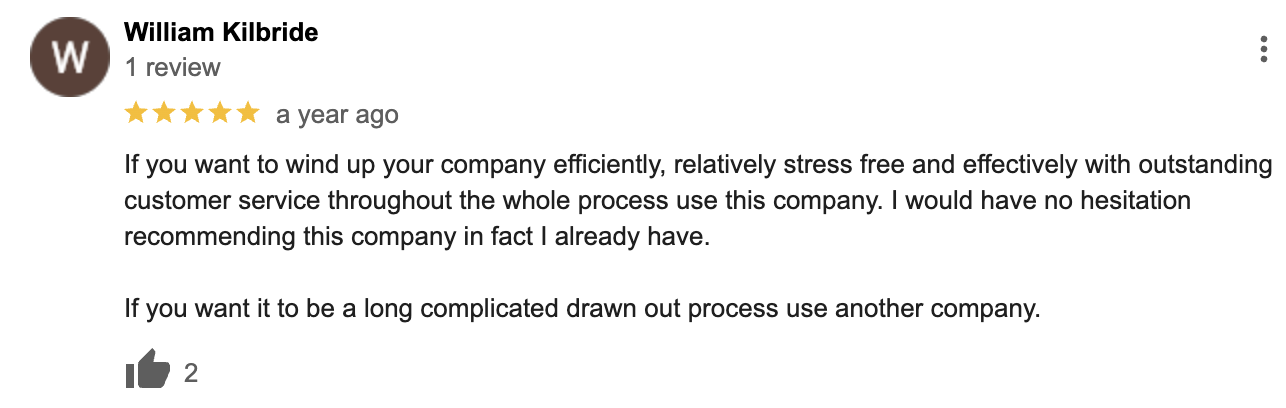

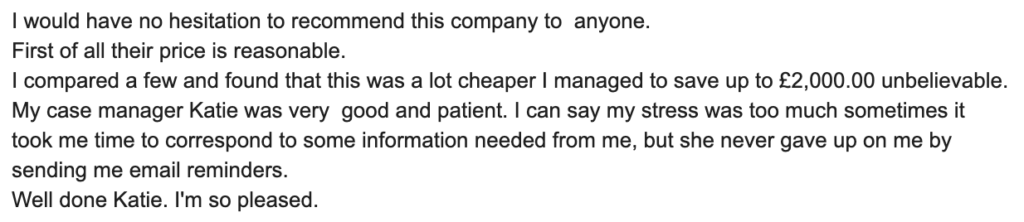

Our Google Reviews

&

Alternatives to Liquidation: A Decision-Making Framework

Liquidation is not always the only or best solution for a struggling business. Depending on your company’s financial situation and future potential, there may be alternative options that allow you to address debts, restructure operations, or even continue trading. This section explores the key alternatives to liquidation and provides a framework for deciding whether they are right for your business.

When Should You Consider Alternatives?

Alternatives to liquidation may be viable if:

- Your business has a realistic chance of recovery with the right financial or operational adjustments.

- You have not yet exhausted all options to negotiate with creditors.

- The company is experiencing temporary financial difficulties rather than long-term insolvency.

Acting early is the key! Waiting too long can reduce the effectiveness of alternative solutions and increase the risk of compulsory liquidation.

Key Alternatives to Liquidation

- Company Voluntary Arrangement (CVA):

A CVA is a legally binding agreement between the company and its creditors. It allows the business to repay debts over time while continuing to trade under the supervision of a licensed insolvency practitioner. This option is ideal for companies with a viable business model but temporary cash flow problems.

Advantages:

- Avoids immediate closure and preserves jobs.

- Protects the company from creditor legal action during the agreement.

- Provides breathing space to restructure operations.

Considerations:

- Creditors must approve the proposal (75% majority by value of debt).

- Failure to meet repayment terms can lead to liquidation.

- Administration:

Administration provides legal protection from creditors while an appointed administrator takes control of the company to restructure, sell assets, or find a buyer. The goal is to maximise returns for creditors while exploring ways to save the business.

Advantages:

- Offers a moratorium, pausing creditor actions.

- May result in the sale of the business as a going concern, preserving operations and jobs.

Considerations:

- Directors lose control of the company during administration.

- Costs can be high, making it less suitable for smaller businesses.

- Informal Arrangements with Creditors:

This involves negotiating directly with creditors to agree on new repayment terms without entering formal insolvency proceedings.

Advantages:

- Avoids public insolvency procedures.

- Can be faster and more flexible than formal options.

Considerations:

- Relies on creditor cooperation and trust.

- Not legally binding, so creditors can still take legal action.

- Time to Pay Arrangements with HMRC:

If your main financial difficulties involve overdue tax payments, you may negotiate a Time to Pay Arrangement (TTP) with HMRC. This allows you to spread payments over an agreed period.

Advantages:

- Helps avoid legal action, such as winding-up petitions from HMRC.

- Flexible terms based on your company’s financial position.

Considerations:

- Requires a clear plan and proof of affordability.

- Non-compliance with the agreement can escalate enforcement actions.

How to Decide the Best Course of Action

Use the following framework to evaluate whether liquidation or an alternative option is most appropriate for your situation:

- Assess the Company’s Viability:

Can the business realistically generate sustainable profits after addressing its financial difficulties? If the answer is no, liquidation may be the better option.

- Analyse Debts and Obligations:

Are your debts manageable with renegotiation or repayment over time, or are they overwhelming relative to your assets and income?

- Engage with Creditors:

Have creditors expressed willingness to negotiate, or are they pursuing aggressive recovery actions, such as statutory demands or winding-up petitions?

- Seek Professional Advice:

A licensed insolvency practitioner can provide an objective assessment of your situation and recommend the most suitable path forward.

Why Alternatives Are Worth Exploring

Choosing an alternative to liquidation can protect your business, preserve jobs, and maintain your professional reputation. However, it’s critical to act early and ensure the solution you choose aligns with your company’s financial and operational realities.

Free Consultation – advice@andersonbrookes.co.uk or call on 0800 1804 933 our freephone number (including from mobiles).

Frequently Asked Questions (FAQs)

When facing the prospect of liquidation, directors often have a range of pressing questions about the process, responsibilities, and outcomes. This section answers the most common questions to provide clear, practical guidance and help you make informed decisions.

1. What Is the Difference Between Voluntary and Compulsory Liquidation?

Voluntary liquidation is initiated by the directors or shareholders, while compulsory liquidation is enforced by the court following a winding-up petition, typically from a creditor. Voluntary liquidation gives directors more control and allows for a more orderly process, whereas compulsory liquidation is often more stressful and public.

2. Can I Stop Liquidation Once It Starts?

Stopping liquidation depends on the stage of the process:

- If voluntary liquidation has been proposed but not finalised, directors or shareholders may explore alternatives, such as a CVA or informal creditor agreements.

- In compulsory liquidation, stopping the process requires legal action, such as disputing the petition in court or settling the debt in full.

3. Will I Be Personally Liable for Company Debts?

As a director of a limited company, you are generally not personally liable for debts. However, personal liability may arise if:

- You signed personal guarantees for loans or credit agreements.

- You are found guilty of wrongful trading, fraudulent trading, or misconduct.

4. What Happens to Employees During Liquidation?

Employees are made redundant when a company enters liquidation. They can claim unpaid wages, holiday pay, and redundancy payments from the National Insurance Fund if the company cannot cover these costs.

5. How Are Creditors Paid During Liquidation?

The liquidator sells company assets and distributes the proceeds in a legally defined order:

- Secured creditors (e.g., those with fixed charges).

- Preferential creditors (e.g., employee wages).

- Unsecured creditors (e.g., suppliers, HMRC).

- Shareholders (if funds remain).

6. What Is a Liquidator’s Role?

The liquidator manages the entire liquidation process, including:

- Selling company assets.

- Communicating with creditors.

- Conducting a review of the directors’ conduct.

- Filing necessary reports and ensuring compliance with insolvency law.

7. How Long Does Liquidation Take?

The process can take anywhere from a few months to several years, depending on the complexity of the company’s affairs, the number of creditors, and the time needed to realise assets.

8. Can I Start a New Business After Liquidation?

Yes, you can start a new business unless you are disqualified as a director. However, using the same or a similar name to the liquidated company is restricted under phoenix company rules, which require specific legal steps to comply.

9. How Much Does Liquidation Cost?

The cost of liquidation varies based on the size and complexity of the company. On average:

- Creditors’ Voluntary Liquidation (CVL): £3,000–£8,000 as a quick guide.

- Compulsory Liquidation: Higher due to court involvement and additional fees.

Liquidation costs are typically covered by the company’s assets or, in some cases, by the directors.

10. What Happens After Liquidation Ends?

Once the company’s assets have been realised, debts addressed, and legal obligations fulfilled, the company is dissolved and removed from the Companies House register. Directors should ensure they comply with any post-liquidation requests, such as HMRC inquiries, and plan their next steps carefully.